Home Equity in a Shifting Market: What You Need to Know

Back in 2011/12, I was trying to sell my home while the market was in the toilet. It took nearly a year to get it sold as I dropped and dropped the price slowly watching all our equity disappear. The market was declining and my price drops were always a little too late. Being in a home you can’t afford is stressful. Being upside down in a home, having to bring cash to the closing table is even more stressful. We ended up selling the home for $20,000 less then we had originally paid for it more than a decade earlier and actually lost $65,000 taking into account the refi that we used to refinish the basement. We were fortunate that we had put a chunk of money down on that house from the sale of a previous home that had appreciated in value giving us a lot of equity. If the house we sold in 2012 had been our first home with a minimum down payment then we wouldn’t have been able to afford to sell the house.

I’m not sharing this to scare anyone. I don’t think we are in a market that is going to plummet like it did after the financial crash of 2008/9. It crashed because of risky lending practices with people not able to afford their ballooning payments leading to massive foreclosures. I do see the market shifting a bit downwards though so I think it’s important to be realistic about home equity.

So what actually is equity in a home and how is it relevant in today’s market?

The equity in your home is the difference between what you owe a lender on the house and what the house will sell for. So, if you are fortunate to have no loan on a house and you can sell it for $300,000 then you have $300,000 in equity. If you owe a lender $250,000 on that same house, you have $50,000 in equity. Equity is not actual money until you sell your home.

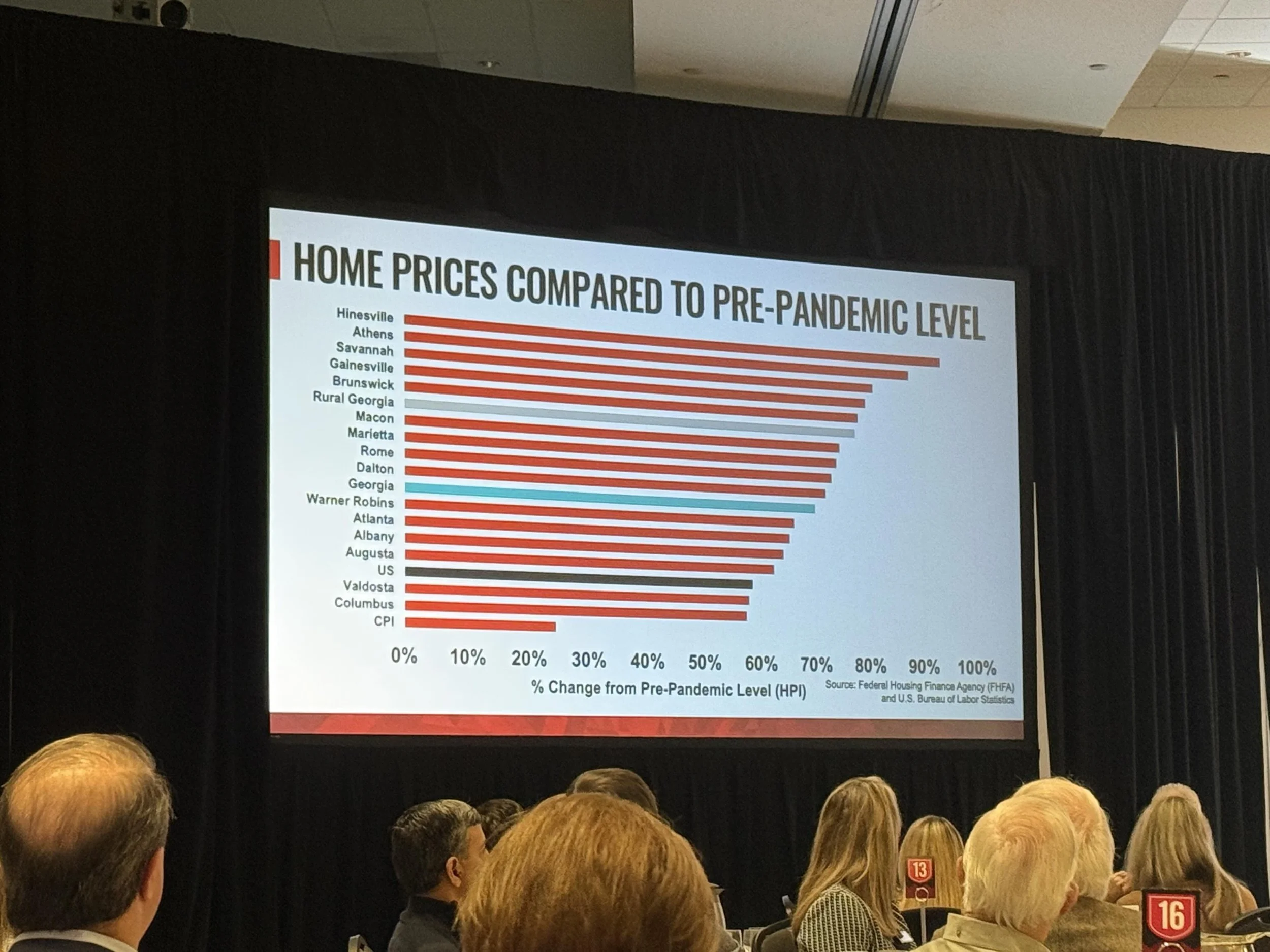

There are three ways to build equity. As you pay each month on your loan, some of that money goes towards what you owe the lender which increases your equity in your home. Another way is to improve the value of the property through renovations or updates. The last way is for the value of the property to increase because of market factors. Since I started selling real estate in 2012, most of my clients have seen their equity grow massively due to property values increasing rapidly. In fact, the Metro-Athens area which includes Oconee county, saw the second biggest jump in Georgia in property appreciation since 2019. Prices have gone up nearly 90%! That’s why for most of my career, if someone had only lived in their home for a year or two, they could still sell the home, pay realtor fees and new loan costs on their next home, and still make money.

Historically homes have only appreciated about 3% per year on average. The 88% increase mentioned above is an 11 to 15% year over year gain. Many of us have come to expect that kind of equity gain. Unfortunately, unless you are significantly improving your property, I think it’s time to recalculate and expect a more normal year over year appreciation and for some areas, your home may have actually lost a bit of value in the last year or so.

Practically what does this mean for you?

Please be careful with home equity lines of credit. I’ve made a video on things to consider.

When you go to sell your home that you haven’t owned very long, you need to be prepared to not actually make a lot of money selling it. Remember, similar to the stock market, you don’t actually realize your equity until you sell your home. So, if you don’t have to bring money to the table and can move to where you want to be instead, consider that a win.

It might not be a great time to think about doing flips unless you can do a lot of the work yourself.

Plan on either being in your home for at least five years (the traditional timeline that equity gain will keep up with selling/buying costs) or be able to rent your home for what your payment is if you do have to move sooner.

Where you buy your home is going to really affect the value. I can try to help you identify areas that look like the prices are still trending up.

Prioritize doing projects in your home that will help you see more appreciation. Visit our Home & Design page for some ideas.

It has been delightful to see clients able to make hundreds of thousands of dollars when selling their homes. This healthy profit has enabled them to buy their next home which also cost hundreds of thousands more than it had a few years previously. The good news of home equity not rising at such astronomical rates is that the next home you are wanting to buy should also not be rising at such a strong pace. This is especially good news for first time home buyers. Prices continuing to rise at the rate they have been would only continue to price people out of the housing market. With home appreciation stabilizing, more people can buy a home which is a good thing.